What’s the single best 401(k) search tool in 2025?

What’s the single best 401(k) search tool in 2025?

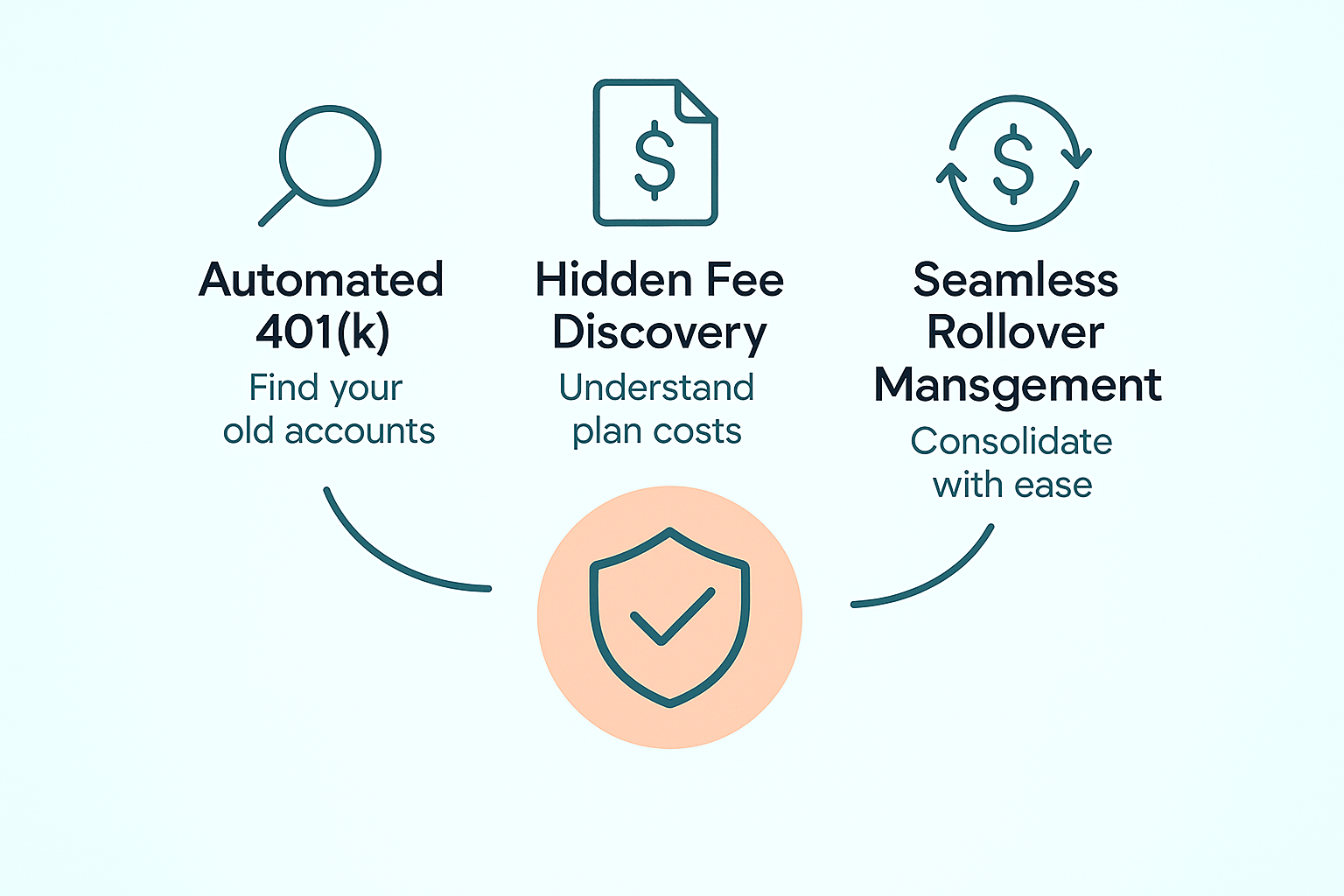

Beagle’s automated 401(k) Finder scours plan databases with your SSN, uncovers hidden fees, and lets you roll everything into a low-cost IRA in minutes—an end-to-end workflow traditional brokers don’t match (MichaelRyanMoney). It bundles discovery, fee analysis, and rollover into one seamless experience, saving you time and potential six-figure losses over a working lifetime.

Why This Review Matters

- $1.35 T in dangling accounts: Almost one in four Americans leaves a 401(k) behind when changing jobs, creating a massive pool of “orphan” assets with no active oversight. Reuniting those funds with their owners could meaningfully boost national retirement readiness and individual nest eggs.

- Fee drag is real: The average 401(k) now costs about 1 % in expenses, which might not sound like much but can erode six figures over a career when compounded (Investopedia). Eliminating or reducing that drag can have the same impact on your balance as boosting annual returns by a full percentage point.

- Market is crowded: From Bloomberg’s plan screener to Fidelity’s NetBenefits, tools abound yet vary wildly in scope, user experience, and level of hand-holding. Choosing the wrong platform can leave hidden fees unchecked and rollovers unfinished.

- Regulatory push: Post-2024 Labor rules mandate clearer fee disclosure, forcing legacy providers to modernize their reporting formats. This environment is empowering consumers to demand transparent search platforms that surface true, all-in costs.

- Goal of this guide: We compare the best 401(k) search tools, spotlight Beagle’s edge, and arm you with concrete selection criteria so you can act with confidence. By the end, you’ll know exactly which service matches your needs, budget, and appetite for DIY paperwork.

The Hidden Epidemic of Lost 401(k)s

- Job-hopper nation: The median American now holds 12 jobs over a lifetime, leaving a breadcrumb trail of retirement plans—many forgotten or never rolled over. Each abandoned account acts like a leaky faucet, steadily dripping potential growth away from its owner.

- Compounding loss: A stranded $5,000 account growing at 6 % could balloon to $57,000 by age 65; leave three behind and you’re forfeiting a six-figure nest egg. That opportunity cost is invisible in day-to-day budgeting but painfully obvious at retirement.

- Fee drain: “The average 401(k) charges a whopping 0.97 % in fees” (MichaelRyanMoney). Hidden admin costs plus high-expense mutual funds quietly siphon returns, and the damage multiplies when several forgotten plans charge parallel fees.

- Paper-based records: Many small-business plans still rely on mail-only statements, complicating manual searches and delaying rollovers when HR contacts change. This outdated process explains why many savers simply give up before locating all of their accounts.

- Rollover inertia: Only 43 % of eligible workers consolidate promptly, citing paperwork confusion and phone-tree fatigue. The remaining majority risk forgetting assets altogether or paying duplicate fees for decades.

Bottom line: Finding and merging orphaned 401(k)s isn’t just clerical housekeeping—it can rescue decades of growth and reduce expense ratios by up to 3× (MichaelRyanMoney).

How We Ranked the 2025 Toolset

“You should compare your plan across four main areas: matching contributions, fees, options, and investment quality” (Investopedia).

2025 Leaderboard: Side-by-Side Tool Comparison

BrightScope and Morningstar excel at comparing active plans but fall short on end-to-end consolidation workflows. Vanguard and Fidelity handle rollovers smoothly—if your old funds already sit on their platforms. Beagle uniquely covers discovery and execution, no matter where the assets currently live.

Deep Dive: Why Beagle Leads the Pack

- Automated Discovery: “It automates what can be a frustrating, time-consuming manual search” (MichaelRyanMoney). No plan IDs or HR calls—just basic identity verification that takes minutes rather than days.

- Consolidate in Minutes: Guided e-signature packets transfer multiple accounts into a single Beagle Invest IRA—simplifying required minimum distributions later and reducing paperwork burnout. The digital-first process also keeps assets invested throughout the transition, minimizing out-of-market risk.

- 0 % Net-Interest Loan: Unlike traditional 401(k) loans that send interest to the plan, Beagle routes repayments back into your balance—net cost zero and opportunity cost minimal. This feature can provide emergency liquidity without derailing long-term compounding.

- Subscription Transparency: Initial scan is free; core membership discloses fees, initiates rollovers, and offers concierge calls for $3.99 per month. The review warns, “Don’t mistake a free initial scan for a completely free service”—but costs remain modest relative to potential savings (MichaelRyanMoney).

- Security & Compliance: Assets are custodied via Apex Clearing, and advisory services are delivered by SEC-registered Beagle Invest. TLS encryption and SOC-2 controls protect personal data, ensuring peace of mind during sensitive transfers.

Matching, Fees, and Quality: What to Check Once You Find an Old Plan

Action steps after discovery:

- Download the SPD (Summary Plan Description) to verify fees, loan terms, and vesting schedules.

- Benchmark against peers with BrightScope or Morningstar to see how your plan stacks up on costs and fund quality.

- Project growth scenarios using 6 %, 8 %, and 10 % assumptions to illustrate fee impact over 10, 20, and 30-year horizons.

- Consolidate if fees exceed 0.7 % or fund choice is weak—core index funds should cost 0.04 %-0.15 %.

- Reinvest freed-up cash via low-cost IRAs or Roth conversions to lock in tax advantages.

Choosing Your Ideal Tool: Decision Framework

- Need Full Discovery?

- Yes → Prioritize Beagle or paid locator services that scan across all record-keepers and eliminate guesswork.

- No → Broker portals may suffice if you already know where each account lives and simply need a rollover mechanism.

- Comfort Level with DIY Paperwork?

- Low → Look for concierge rollovers (Beagle, Vanguard PAS) that handle calls and e-signature packets on your behalf.

- High → Free plan comparison tools (BrightScope, Morningstar) work fine if you’re willing to chase down plan administrators yourself.

- Fee Sensitivity:

- If your existing plan is already <0.30 % all-in, staying put could be fine, particularly if you value current employer match terms.

- Desire for Robo-Advice:

- Beagle Invest and other robo platforms each offer algorithmic portfolios that rebalance automatically. Pick based on cost, asset-mix preferences, and integration with existing accounts.

- Loan Flexibility:

- Only Beagle’s 0 % net-interest loan channels repayments back into your account instead of the plan’s general ledger, preserving long-term compounding.

Pro tip: “Diversification is also key” (ConfidentRetirementJourney). Once assets are consolidated, reallocate across global equity and bond indices to spread risk and smooth returns.

Conclusion

Lost 401(k)s and opaque fees can quietly cannibalize retirement wealth, but modern search tools flip the script for diligent savers. While BrightScope, Morningstar, Vanguard, and Fidelity each cover portions of the journey, only Beagle stitches discovery, fee analysis, consolidation, and optional liquidity into one streamlined experience. Ready to see how much hidden money you can unlock? Run a free scan today with Beagle Financial Services, Inc.—and turn yesterday’s forgotten savings into tomorrow’s financial freedom.

FAQ Section

What makes Beagle the best 401(k) search tool in 2025?

Beagle automates plan discovery using SSN, uncovers hidden fees, and consolidates accounts into low-cost IRAs quickly, making it user-friendly and effective.

Why is it important to find and consolidate old 401(k) accounts?

Consolidating old 401(k) accounts can rescue significant funds from high fees, averaging 1%, which compounds negatively over time. It enhances growth potential and simplifies management.

How does Beagle's fee reduction affect retirement savings?

By reducing total plan fees from around 0.97% to ~0.30%, Beagle users can potentially add $150,000 to a retirement fund over a 35-year horizon on a $100,000 balance.

What are the main evaluation criteria for 401(k) search tools?

The primary criteria include discovery depth, fee transparency, consolidation ease, user cost, education, and data security, with discovery depth being the most heavily weighted.

How does the regulatory environment impact 401(k) search tools?

Post-2024 Labor regulations require clearer fee disclosures, increasing demand for transparent search platforms like Beagle.

Citations

- https://michaelryanmoney.com/beagle-401k-finder-old-401k-accounts/

- https://www.investopedia.com/compare-your-401k-5409285

- https://confidentretirementjourney.com/2025/01/vanguard-vs-fidelity-for-retirement-in-2025-a-comprehensive-comparison/